Rent Paid on Time, Penalized Anyway

Why can a rent payment be timely under the lease and still create a costly VAT problem?

Paying rent on time protects you from default. Paying from a compliant invoice protects you from additional exposure to occupancy costs.

Controlling occupancy costs starts before the first invoice is paid. It starts with reviewing lease language before the lease is signed and making sure the payment process can support the legal, tax, and operational requirements that follow.

As lease administrators, one of our core responsibilities is making sure rent is paid on time and accurately. We understand that a missed or late rent payment can result in late fees, default, and even the forfeiture of lease options. But in global lease administration, paying rent on time is not always enough.

In countries where commercial rent is subject to value-added tax (VAT), a rent payment can be timely under the lease and still create a compliance consequence. International rent payments trip up many companies, not because they do not understand the law, but because the process is often managed in silos within the organization.

Paying rent across borders is not simply “wiring the payment.” You may be dealing with multiple currencies, withholding taxes, VAT, local invoice requirements, entity registrations, locally trapped cash, central bank requirements, foreign exchange rules, and e-invoicing mandates.

This post focuses on VAT compliance, but the bigger lesson is that lease administrators need to understand how non-income-based taxes (NIBT) and local regulations are handled within their companies, as well as the nuances of each country. We do not need to be tax experts, but we do need to understand the components that directly impact payments and maintain a playbook for each country we operate in. We need to ask better questions and work with the right stakeholders before the issue affects the P&L. This is another area where you can add value to your company and help control occupancy costs.

A rent payment can be correct from a lease perspective and still fail from a VAT compliance perspective.

Just because VAT appears on an invoice doesn’t necessarily mean it is recoverable.

Input VAT generally depends on having a valid, compliant VAT invoice. If the invoice is wrong, incomplete, issued to the wrong legal entity, missing required VAT data, or not transmitted through the required local platform, the VAT recovery may be delayed or denied. There are also local requirements that impact VAT recoverability. For example, in the UK, commercial rent is generally VAT-exempt unless the landlord has opted to tax the property. In India, commercial rent may involve GST treatment and reverse-charge considerations depending on the parties and registration status. Lease administration should identify these requirements at the beginning of the lease and confirm the process with tax, NIBT representatives, or documented company policies.

This is why lease administration, AP, tax, legal, and accounting need to maintain open communication and regular touchpoints. AP may be focused on payment approval. Lease administration may be focused on whether the amount matches the lease. The tax focus may be on whether the invoice supports VAT recovery. Accounting may be focused on whether VAT is recorded correctly. All of those controls matter, but if they are not connected, the organization may pay the landlord correctly and still fail the tax compliance requirement.

What Makes a Rent Invoice VAT Compliant?

The exact requirements vary by country, but here are some examples: (always consult your company’s tax or NIBT representative)

- Correct landlord legal name and address

- Correct tenant legal entity and billing address

- Supplier VAT registration number

- Customer VAT registration number, when required

- Unique invoice number

- Invoice date and tax point, if applicable

- Rental period covered

- Taxable amount before VAT

- Correct VAT rate and VAT amount

- Total amount due and currency

- Required e-invoice format or local platform submission

That last item is becoming increasingly important. In some countries, the invoice is no longer a PDF attached to an email. It may need to be issued through a government platform or an approved e-invoicing channel to ensure proper tax treatment.

Mini Case Study

I have presented case studies in the International Lease Administration track at the National Real Estate Tenants (NRTA) conference. This is a mini version of one scenario that illustrates the consequences of non-recoverable VAT.

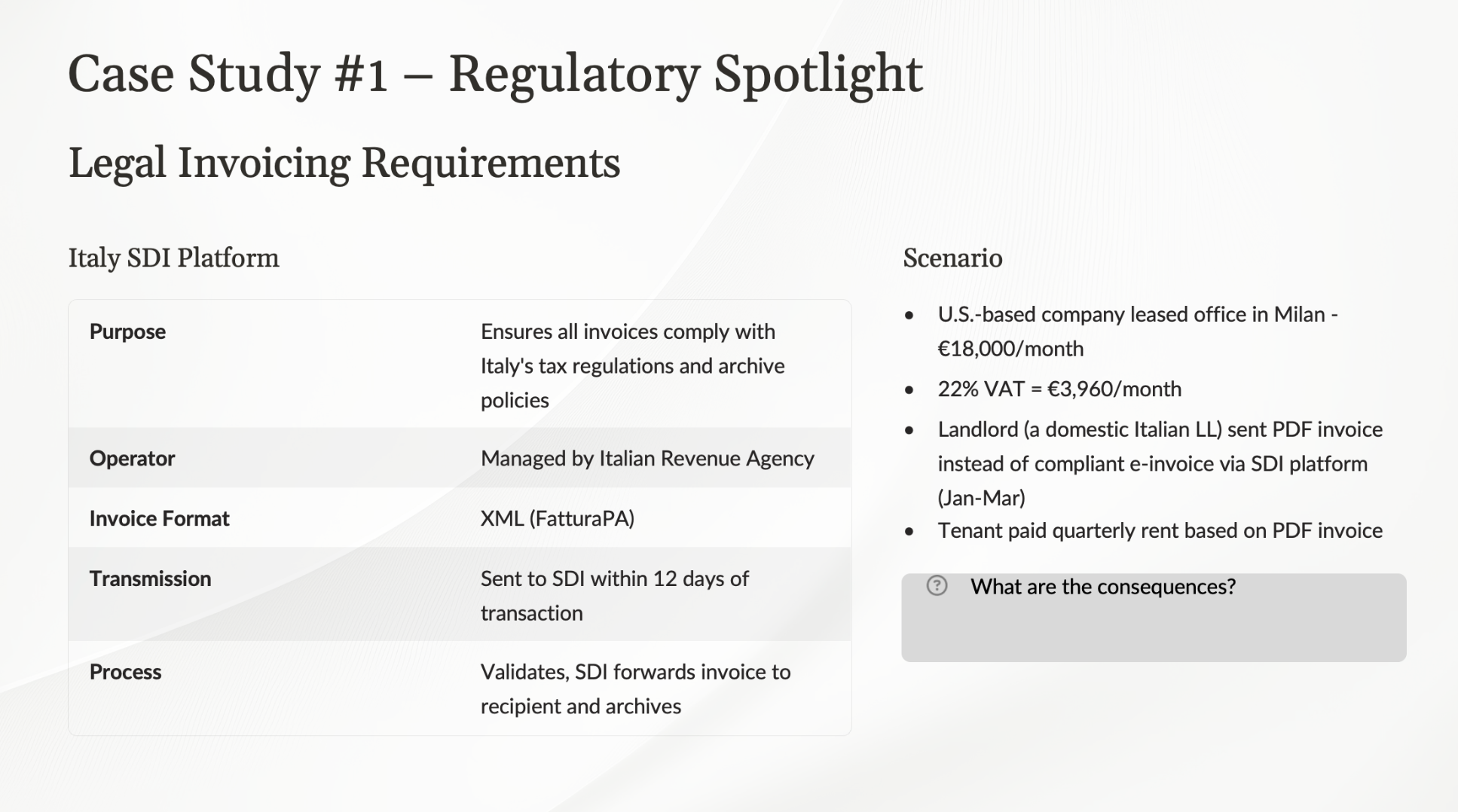

Case Study Facts

A U.S.-based company leases an office in Milan. Rent is €18,000 per month, paid quarterly. VAT is charged at 22%, or €3,960 per month.

The landlord sends a quarterly PDF invoice by email for January, February, and March. The tenant pays on time based on the invoice received.

From a lease administration perspective, the invoice matches the lease, and the rent payment is approved and paid.

But there was a problem. The landlord should have issued the invoice through the required local e-invoicing process. Instead, the tenant paid from a PDF invoice that did not meet the local invoice compliance requirement.

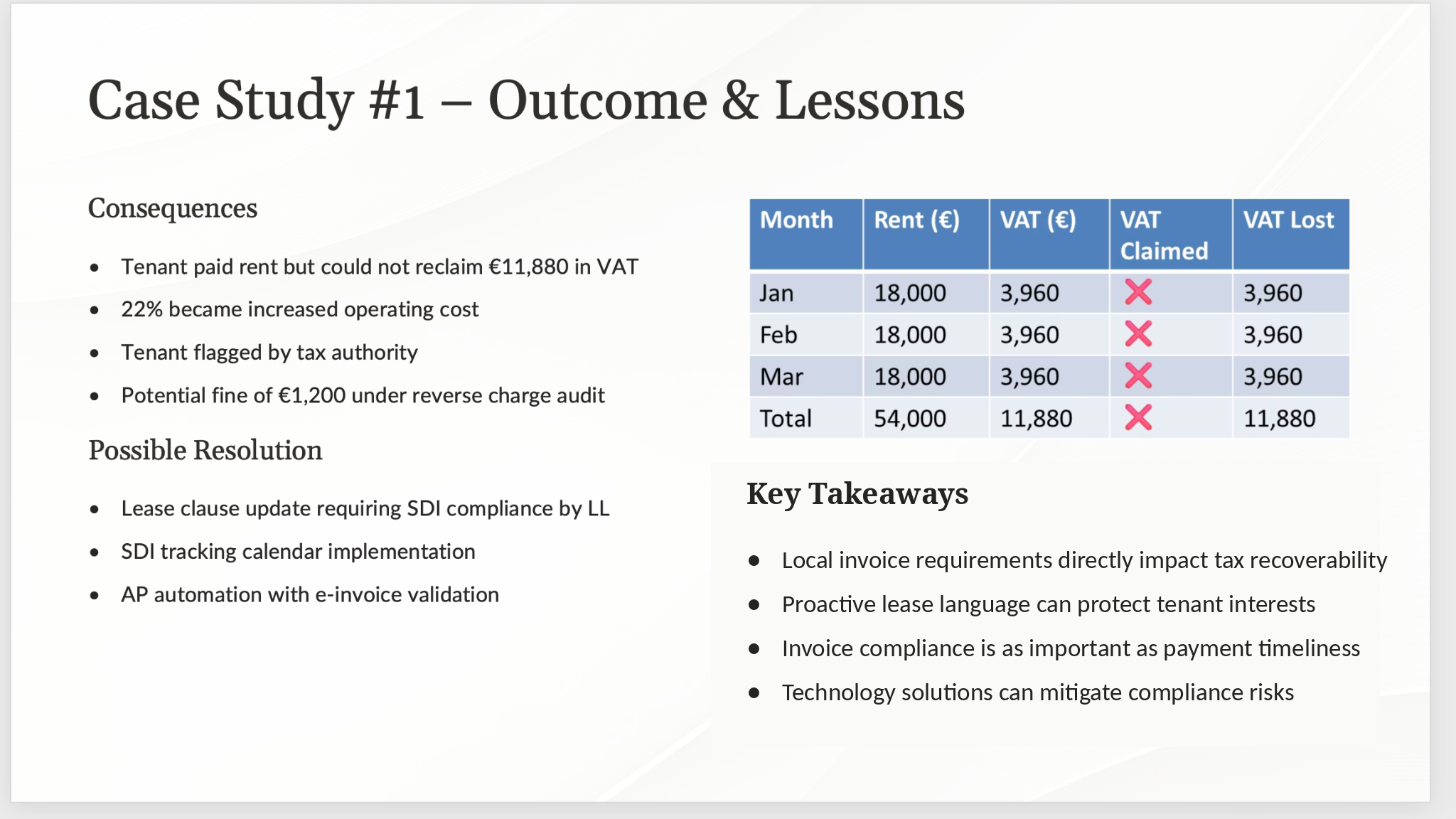

The tenant paid €54,000 in rent and €11,880 in VAT. Outcome of the tax audit, the tenant could not recover VAT. Tenant may also be subject to a statutory fine.

That 22% VAT became an additional occupancy cost because the cost must be expensed and becomes an unexpected hit to the P&L.

The Lease

This is where the issue becomes a real conundrum.

I have argued with many landlords on this issue, and it can be a tough argument to win after the lease is signed. The landlord’s position is usually simple: the lease says rent is due on “x” date, and they expect to be paid.

They may not care whether the tenant can recover VAT, nor whether the invoice creates an internal tax issue. They will often point back to the payment clause in the lease and try to hold the tenant to it.

This puts the tenant in a difficult position. If you hold payment while waiting for a compliant invoice, the landlord may assess late fees or even claim default. Default can trigger additional consequences such as loss of lease options. If you pay from a noncompliant invoice, you may lose the ability to recover VAT. When I was a new lease administrator, I thought, from a logical standpoint, that the landlord could not charge a late fee if they did not follow the regulations, but I learned it is not always that simple. Either way, the rent expense just became more expensive. The cost may show up as a late fee or as VAT that should have been recoverable but now has to be expensed. There could also be statutory penalties. On the surface, it might seem like a simple cost-benefit analysis, but it is not always that simple either. Those early experiences taught me the importance of understanding the tax basics, being proactive, collaborating with the right stakeholders, and improving our processes before the issue impacts the P&L.

I was involved in a situation where we were holding rent while waiting for a VAT-compliant invoice. The landlord was holding firm that the lease did not require him to provide a VAT-compliant invoice, and e-invoicing was not yet mandatory in this country. Add to that, we were in the middle of lease renewal negotiations. The important point of this situation is not operating in a silo; there is a broader financial picture that involves multiple stakeholder groups, so we remain compliant with the law, maintain our relationship with the landlord, and achieve the best possible financial outcome given all the variables. In the end, we paid the rent that was due without a VAT-compliant invoice, immediately expensed the VAT to avoid incurring local statutory penalties, but we were successful in including language in the renewal requiring the LL to provide a VAT-compliant invoice. It was an early renewal, so it was structured so that the language became effective at full execution. It was a business decision to forgo VAT recovery to secure favorable renewal terms, maintain our relationship, and correct the problem going forward.

Your Lease Language Is Your Best Protection

The most proactive way to manage this risk is to address it in the lease before the first invoice is ever issued, and this is just another reason I preach that lease administration should have a seat at the table. They understand what is required to administer the lease and remain compliant and know which stakeholder to engage.

The lease should require the landlord to provide legally required invoices in the proper format, with the required VAT information, and through the required local platform or process. This should include e-invoicing platforms, government portals, XML formats, VAT invoice requirements, reverse-charge language, or any other jurisdiction-specific invoicing requirement.

This should not be treated as an administrative preference. It should be a lease obligation.

The lease should also address what happens if the landlord does not comply. Can payment be withheld until a compliant invoice is received? Does the payment due date run from receipt of a compliant invoice? Is the tenant protected from default, late fees, or denied VAT recovery caused by the landlord’s failure?

The tenant should not have to choose between paying rent on time and preserving VAT recovery.

Where do you see the biggest VAT compliance challenge: landlord invoice quality, e-invoicing platforms, AP workflow, entity mismatches, or lease language?

Disclaimer: This article is intended as general information to help prompt internal review, process improvement, and stakeholder discussions. VAT, GST, withholding, e-invoicing, and local invoicing requirements vary by jurisdiction, entity, and fact pattern. Validate requirements with your company’s tax, legal, NIBT, accounting, and other appropriate stakeholders before making payment, lease language, or process decisions.

I host a private LinkedIn group dedicated to lease administrators and lease accounting professionals. It is a space to share ideas, ask questions, and learn from others managing similar challenges across different industries and geographies. I truly believe we are stronger when we share experiences.

Request to Join →